Engagements to report on summary financial statements

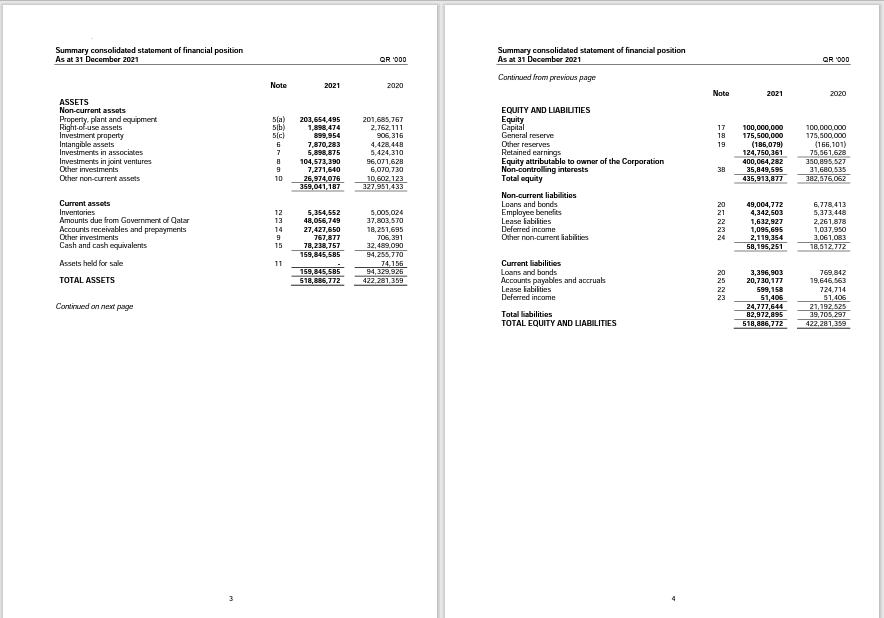

Summary financial statements is historical financial information that is derived from financial statements but that contains less detail than the financial statements, while still providing a structured representation consistent with that provided by the financial statements of the entity’s economic resources or obligations at a point in time or the changes therein for a period of time. Different jurisdictions may use different terminology to describe such historical financial information. Example of summary financial statements ( Summary statement of financial position ) is presented below. Considerations related to the audit of summary financial statements engagement. The auditor shall accept an engagement to report on summary financial statements only when the auditor has been engaged to conduct an audit of the financial statements from which the summary financial statements are derived. Before to accept an engagement to report on summary financial statements, the auditor...